Building a defensive income portfolio

Where to look for income in difficult times

Sustaining a level of income during the current difficult climate, is a challenge facing many investors.

The typical source of income in more prosperous times, equity income, has dried up, so people are forced to look elsewhere.

One asset class that has been pushed to the fore in recent weeks is investment trusts, as these are in a better position to pay dividends than conventional equities.

Other, more esoteric assets are being considered, such as infrastructure, as well as bonds.

But each asset class comes with its own risks, and nothing is a straightforward, no-strings investment.

In this report, we look at how income investors can address the challenges of the current climate.

With the yield on the two year UK government bonds having reached negative levels this week, and the longer-dated ten year bond presently 0.2 per cent, the income from those assets have dropped below the prevailing rate of inflation.

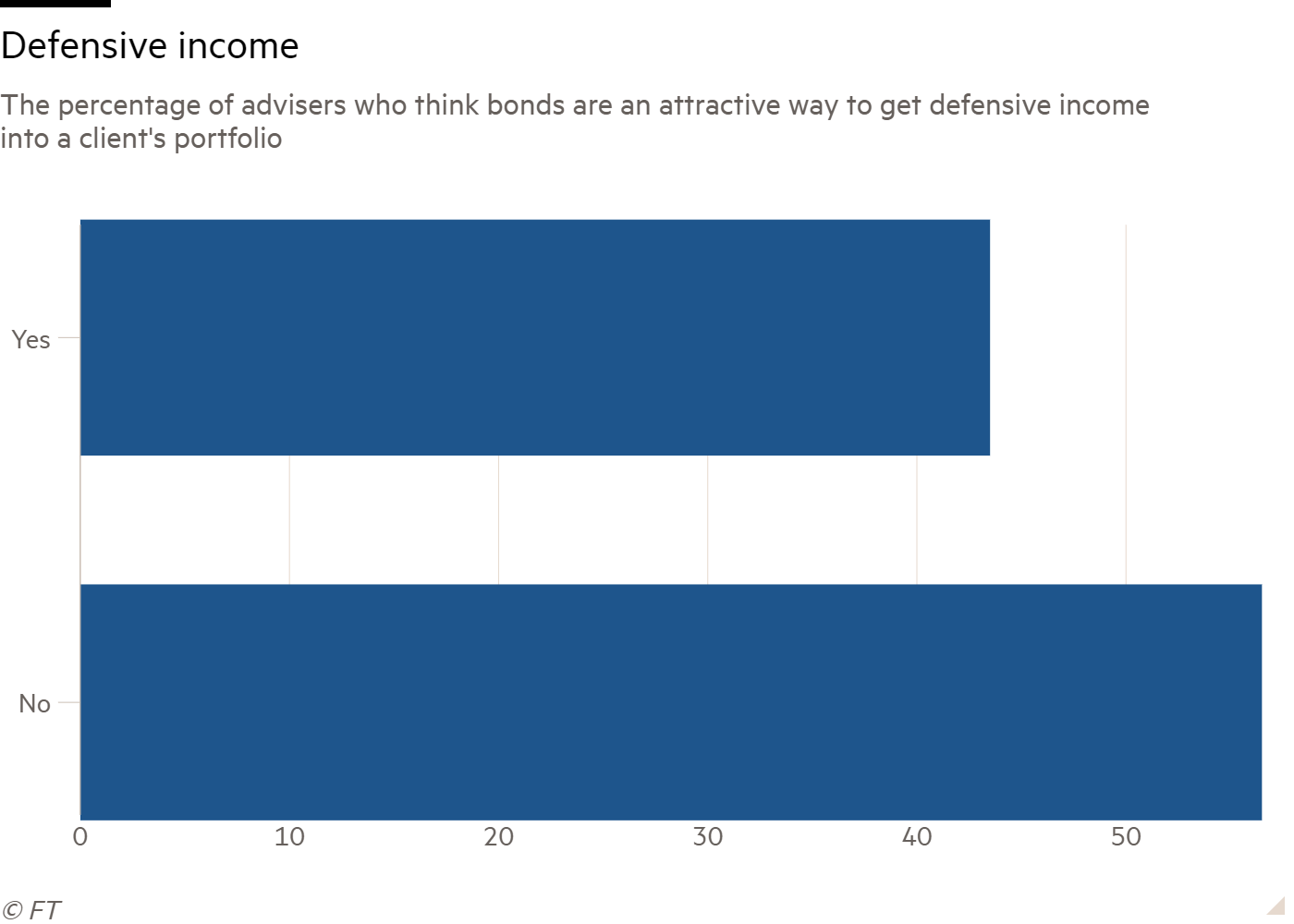

Of those advisers who responded to the FTAdviser poll, 56 per cent said bond are not an attractive way to get defensive income into a client’s portfolio right now.

Bond yields have been pushed lower over the past decade by the central bank policies of quantitative easing, whereby the banks buy government bonds at any price, in order to force the yields lower, making it cheaper for governments to borrow, and improve the liquidity of markets as a whole.

This bond buying programme drives the prices up, and the yields down, and so the income available for clients is reduced.

This has prompted many advisers to look elsewhere for defensive income.

But Alex Harvey, co-head of research and portfolio manager at Momentum Global Investment Management said it was still possible to get a decent yield from a bond portfolio.

He said: “Investors seeking an income from their portfolio are well placed today to benefit from the recent market chaos.

"Credit spreads on higher quality and short maturity corporate bonds skyrocketed in March and two months later still offer good value.

"A blend of investment grade, high yield and emerging market bonds should yield around 5 per cent today and we would favour using an active manager for higher risk corporate exposure.

"These could be combined with some higher yielding and still discounted fixed income investment trusts and some high-quality dividend paying equity names in more defensive sectors.”

Generating income in a challenging environment

Words: David Baxter

Images: Fotoware

“Lower for longer”, a term commonly used in the context of interest rates, is becoming an increasingly fitting catchphrase for dividend investors.

With the coronavirus sending shockwaves through the global economy and businesses attempting to navigate enormous uncertainty, many companies have decided to cut, suspend or cancel their dividend altogether.

This has been most obvious in the UK equity market, traditionally popular for its high yields. Some of the market’s big payers, such as Royal Dutch Shell and BT, have cut their dividends for the first time in decades.

The UK’s major banks, a big source of income, suspended their payouts in the face of pressure from the Prudential Regulation Authority.

The fact that so much of the dividend stream in the UK stems from a handful of big payers means these developments have been extremely challenging for income-oriented clients. And the pain is likely to continue.

In the UK, Link Asset Services predicts that 2020’s dividend payments could be down by between 27 and 51 per cent from 2019’s £98.5bn total.

With equities forming a core element of many income portfolios, clients in decumulation have few places to hide.

Many income-paying stocks will simply deliver less than they normally would, with a knock-on effect for open-ended equity income funds which can only distribute the dividends they have received from holdings.

Many income-paying stocks will simply deliver less than they normally would, with a knock-on effect for open-ended equity income funds

Those with a broader remit, from multi-asset income funds to discretionary fund managers (DFMs), are also feeling the pain.

Perhaps more worryingly, dividends may simply be lower in future as companies look to “rebase” their payouts to a more sustainable level.

Royal Dutch Shell, for one, has radically reset the level of its dividend payments by enacting a two-thirds cut.

As prudent as such decisions might seem, they mean that those looking to generate a sustainable, defensive and sufficient income will need to be highly selective in the equity space, and consider other asset classes. Options are still available to income investors, but each comes with a trade-off.

Taking stock

In the short term, some investors will be able to maintain their current level of income using equity investment trusts.

Unlike open-ended funds, investment trusts can put up to 15 per cent of each year’s income into a revenue reserve. This reserve serves as a rainy day fund, used to top up dividend payments in difficult markets.

Investment trusts can put up to 15 per cent of each year’s income into a revenue reserve

UK equity income investment trusts tend to have substantial reserves. Analysis by Investec Securities found that, of 17 selected trusts in the sector, all but one had enough revenue reserves to cover at least six months’ worth of the last annual dividend payment, as of the end of March.

Many of these trusts also have long records of increasing their dividend each year: City of London has the longest stretch, having increased its payment for 53 consecutive years.

This offers some reassurance, because it suggests trusts’ boards will want to maintain a reputation as a stable source of rising income.

However, there are drawbacks. Some trusts with a seemingly secure dividend are seeing their shares perform well, meaning investors may have to pay above the odds to get exposure.

Shares in City of London, which has again increased its dividend this year, traded at a 2 per cent premium to the value of underlying assets on 11 May, according to Winterflood data.

Reserves will only go so far

That said, not every trust in the sector looks expensive. The average UK equity income trust, as categorised by Winterflood, traded on a 6.6 per cent discount on 11 May.

But this may simply reflect problems in the UK market, and the fact that even revenue reserves cannot protect these trusts from longer-term trends.

Like companies, many trusts could well rebase their dividends to a lower level in the anticipation of more trying conditions over the next few years.

Many trusts could well rebase their dividends to a lower level

The board of Troy Income & Growth will maintain the trust’s quarterly dividend rate of 0.695p for the rest of this year, but warned it was “almost certain” the dividend would be cut in 2021.

This stemmed partly from the fact that the managers had already started moving the portfolio “away from higher yield but low growth, to lower-yielding and higher-growth investments”, but predominantly related to coronavirus-induced uncertainty.

Others are also managing expectations. The board of Temple Bar Investment Trust has declared that while it would maintain the first interim dividend of 2020 at the previous year’s level, shareholders “should not assume from this that the total dividend for the year as a whole will be similarly maintained”. Clients relying on this sector for income may receive less money in the longer term.

Further afield?

Further down the line, defensive and selective UK equity income managers such as Troy’s team could reward investors by providing a growing income and some level of protection from future volatility.

But investors who need to maintain a sufficient income right now may want to consider overseas equities. Here, yields often tend to be lower than in the UK, but diversification should at least aid investors.

The table below shows how open-ended equity income funds looked in terms of aggregate yields at the start of 2020.

This gives an impression of how other markets compared with the UK at the time. With share prices having fallen dramatically in February and March, some funds’ stated yields may now look much higher, but could prove unreliable given the current economic uncertainty.

Those with income-oriented clients could well turn to global equity income funds or a range of equity income funds outside the UK.

Once again, some investment trusts have impressive levels of revenue reserves. But they could also be hit by a sustained fall in dividends: Janus Henderson has predicted that global dividends could fall by between 15 and 35 per cent this year.

Alternatives

Fortunately for investors, stable yields similar to those once on offer from UK equities can be found in alternative asset classes, which are often best accessed via investment trusts because of their limited liquidity.

But not all areas are holding up in the current crisis, and those that have proved resilient may seem expensive.

Some areas which once offered good yields have been hit hard: mainstream property trusts have struggled to collect their entire rental income. Debt-focused trusts have also struggled, as have those focused on leasing, which tend to deal with airports.

Around 30 trusts have either cut, suspended or cancelled their dividends or made warnings about future payouts since the onset of the crisis, and more than two thirds of them sit in these three sectors.

One area that has been broadly unaffected is the infrastructure sector. Infrastructure assets, from schools to power plants, will broadly continue to operate and pay their rents as normal, and trusts in the sector continue to generate attractive levels of income.

But here, those managing client money need to consider what they will pay for a secure income, because infrastructure trust shares tend to trade at expensive levels. The average generalist infrastructure trust’s shares, as categorised by Winterflood, traded at a 7.7 per cent premium to underlying assets on 11 May.

Back to bonds?

Many fixed income allocations have paid off this year, because government bonds performed strongly as equity markets tanked in February and March. But investors may also be tempted to reconsider corporate bonds as a source of income.

The strong performance of bonds in recent years has made it hard to generate much income from them without taking significant levels of risk

With yields moving inversely to prices, the strong performance of bonds in recent years has made it hard to generate much income from them without taking significant levels of risk.

But with equity volatility rippling out into the corporate bond space earlier this year, yields have looked much more attractive than they once did, even after prices recovered somewhat in April.

And with the Federal Reserve embarking on a significant programme of bond buying, fixed income has a level of technical support.

The main problem with using bonds for income is that investors still need to delve into higher-octane parts of the universe if they wish to find the yields associated with UK equities.

US investment grade bonds, a safer part of the corporate debt market, recently yielded around 2.5 per cent in sterling terms – nowhere near the yields of more than 4 per cent historically available in the UK stockmarket.

Investors still need to turn to high yield or emerging market debt for better yields, and though these look attractive there are plenty of risks.

The US high yield bond market, for example, is heavily exposed to the energy sector and the effects of a whipsawing oil price. Similarly, emerging markets could be in for a rocky period as some countries struggle to deal with the pandemic.

Some dedicated high yield and emerging market debt funds can ride out the volatility of their respective asset classes by being both selective and flexible in their approach.

In emerging markets, for example, funds that invest across different types of debt, taking in both government and corporate bonds either in local currency or a “hard” currency such as the US dollar, look best positioned to deal with uncertainty.

Similarly, investors who wish to diversify their income approach into the bond universe might favour strategic bond funds.

Some of these target attractive levels of income, often by making big allocations to high yield bonds. But their ability to invest across the bond universe means they can, in theory, offset these risks with more defensive holdings.

One answer may be to diversify across a series of these asset classes. But in difficult times for income investors, yield will often come with some kind of price.

What are the income opportunities available in credit?

Generating returns from income looks set to remain challenging for investors.

Government bond yields are expected to remain low for some time given the scale of monetary and fiscal stimulus being implemented across the world.

Equity dividends are being cut, as company revenues and earnings decline, or because central banks or governments require this in order to extend certain loan arrangements.

The challenge facing income investors

The chart below shows just how much lower yields on global government bonds and equities are compared to credit markets.

Global investment grade now yields 2.8 per cent, versus 0.4 per cent on government bonds, 2.7 per cent on the Euro Stoxx 500 and 2 per cent for the S&P 500, while global high yield (HY), which is the riskier end of corporate bonds, yields more than 8 per cent in aggregate.

This gap may also be set to widen with equity dividend futures in the US and Europe currently predicting dividends will decline by between 25 per cent and 50 per cent.

With little income on offer in the government bond or equity markets, it seems inevitable investors will increasingly look to the credit market for opportunities.

We believe there is currently a window of opportunity for investors given historically high corporate bond spreads, which underlines the attractiveness of yields in credit compared to other markets.

A corporate bond spread reflects the excess yield over a lower risk, similar maturity government bond, so a higher spread implies better value.

Spreads likely to “normalise” before year-end

The below charts illustrate how wide credit spreads are at the moment. The sharpness in their rise over the lasts six weeks is unprecedented and shows just how severe a recession the market is pricing in.

These levels are also unsustainable, or at least they have been in the past, as the charts also demonstrate.

While there is likely to be more stress ahead of us (so we could see further sharp moves up or down in spreads), we also believe these exceptionally elevated levels will likely only last up to two quarters before returning to more normalised levels. Ultimately, this move will likely be driven by a change in sentiment and could well be quite rapid.

As well as the potential for income returns, there is also the added element of potential price appreciation, since bond prices rise as yields and spreads fall.

Historically, from the current spread levels on US dollar investment grade (IG) bonds, which are regarded as lower risk and higher quality, of 200 basis points (bps), the excess return over government bonds in the proceeding three years has averaged about 9 per cent annualised.

For US dollar high yield (HY), the current spread of between 700-800bps, has been followed by annual excess returns of 18 per cent over three years, and 30 per cent over five years.

What about defaults?

While the return prospects are attractive, there is nevertheless the likelihood that defaults will rise given the stress in the market.

This increased and very real risk is part of the reason yields have risen so much. We believe, however, that the rate of defaults implied by market levels has gone too far.

The historical average five-year default rate for global IG has been 0.9 per cent; based on the current level of spreads, US IG now has an implied default rate of 8.7 per cent. For the HY market, the historic average default rate is 14.6 per cent compared to a currently implied 37 per cent.

Which areas look attractive?

While we expect a decline in global GDP by 3 per cent, there will still be winners in this crisis situation.

Retailers with convenience store footprints, for example, are seeing increased demand as social distancing in many countries is preventing people from eating out in restaurants and travelling far for their groceries.

The importance of telecommunication services has increased significantly. With the rising number of people working from home, demand for broadband services has risen and we have seen a number of telecommunication businesses become more profitable.

As individuals and households are unlikely to change broadband providers, telecoms providers have seen a reduction in marketing costs and less customer “churn”.

One might expect reduced power demand from the industrial sector to have a negative impact on utility companies, but power demand from the private and residential sector, which pay higher prices, is up.

Also, power companies’ revenues are no longer solely linked to power volumes; they are also linked to service contracts.

So for the most part, we expect revenues for utilities will be relatively stable.

Then there are the more vulnerable companies who have had to effectively hibernate, in some cases halving or virtually wiping out revenues.

We have seen some instances of businesses with strong underlying operations and sizable assets, issuing new bonds with very attractive yields.

There are numerous companies within the leisure, hotels, airlines and transportation sectors struggling to cover their operating costs.

As these companies start to run out of liquidity they will have to turn to central banks, government programmes or the financial markets.

Window of opportunity

The income opportunity set in global credit has expanded significantly over the past few weeks.

Credit spreads are at historic highs, offering yields that neither the equity market nor the government bond market can match.

In the past, these levels have preceded attractive returns, but we think investors probably have a relatively short window of opportunity to take advantage of these dislocations in the market.

Patrick Vogel is head of credit Europe at Schroders